Asia is the largest continent with a remarkable 60% of the world’s population. This diverse and dynamic continent has borne witness to several economic booms, including the Japanese economic miracle, the resounding growth in China and India, the awe-inspiring transformation along the Hun River in South Korea, and the emergence of the Tiger Cub economies. Additionally, Asia maintains its reputation as the fastest-growing economic region. This article will explore the economic prowess demonstrated by the top 10 largest economies in Asia. We take a closer look at these economies through the IMF’s latest World Economic Outlook (October 2025).

List of the top 10 largest economies in Asia

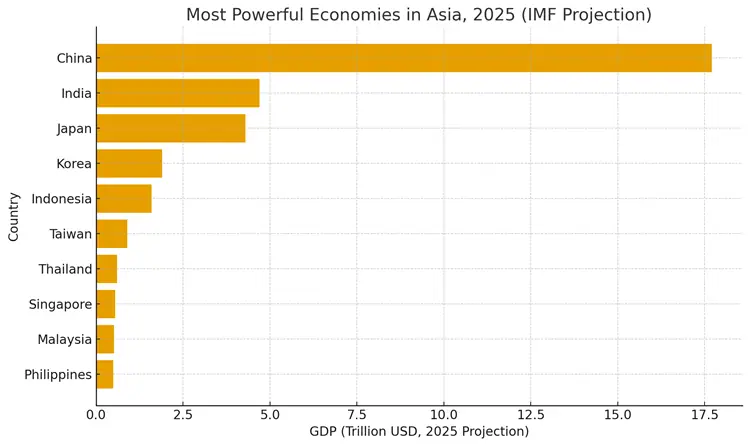

The top 10 largest economies in Asia are China, India, Japan, South Korea, Indonesia, Taiwan, Thailand, Singapore, Malaysia and Philippines.

China, the largest economy in Asia

China’s role as Asia’s anchor economy remains unquestioned, yet the mood surrounding it feels markedly less confident. The IMF expects growth of 4.8% in 2025, slipping further to 4.2% in 2026 — numbers that would have seemed unthinkably low a decade ago. It also tops the list of the most powerful countries in Asia.

The reasons are familiar but persistent. The property sector remains in distress more than four years after the bubble burst. Investment continues to fall, and the hoped-for stabilisation keeps slipping further into the future. Some analysts even warn of a creeping debt-deflation cycle. Add to that the continuing bite of US tariffs and the limits of state subsidies for manufacturing — once China’s favourite growth lever — and the outlook looks complicated. Subsidies that once fuelled expansion are now distorting markets and misallocating capital, dampening the productivity gains Beijing badly needs.

India, 2nd most powerful economy in Asia

India’s story, meanwhile, offers an almost cinematic contrast. The IMF projects GDP growth of 6.6% in 2025 and 6.2% in 2026, putting it among the world’s fastest-growing major economies. Inflation, surprisingly, has been lower than expected — a rare case in today’s overheated global environment — suggesting that consumer demand, while strong, hasn’t tipped into unsustainable territory.

Even more telling is India’s fiscal discipline. Its projected primary deficit for 2025 is smaller than before the pandemic, something very few large economies can claim. There’s still room for scepticism — inequality remains high and job creation uneven — but India’s resilience stands out in a region struggling to keep its footing.

Japan

Japan continues its slow-and-steady path, which may sound dull but is arguably a success story in its own right. The IMF forecasts growth of 1.0% in 2025 and 0.8% in 2026. Behind these modest figures lies a solid current-account surplus — nearly 5% of GDP in the first half of 2025 — cushioning it from external shocks.

The Bank of Japan is also inching away from its long-standing ultra-loose monetary policy. Rates are rising, cautiously, but the shift is more psychological than dramatic. The real test will be whether this policy normalisation can happen without snuffing out fragile domestic demand.

South Korea

South Korea’s story feels more balanced — and more uncertain. Growth of around 2% in both 2025 and 2026 suggests steadiness, but the country’s heavy reliance on global chip and tech exports keeps it tied to external moods. Inflation, at 2%, is right where policymakers want it.

Interestingly, the IMF draws on South Korea’s industrial policy of the 1970s as a historical lesson in getting state intervention right — precise targeting, steady macro management, and pragmatic execution. It’s a subtle reminder that not all industrial policy is equal, and that past success doesn’t guarantee future resilience in a more fragmented global economy.

Indonesia

Indonesia, the region’s heavyweight, is projected to hold steady at 4.9% growth in both 2025 and 2026. Inflation stays low, rising from 1.8% to just under 3%. These numbers suggest a healthy economy, but perhaps one cruising below its potential. Infrastructure investment continues, yet red tape and policy uncertainty may be quietly trimming what could otherwise be faster progress.

Taiwan

Taiwan’s economy, deeply embedded in global supply chains, faces the dual pressures of geopolitical tension and market volatility. Growth is projected at 2.9% in 2025, easing slightly to 2.1% in 2026. Inflation remains subdued at below 2%. Stability, yes — but perhaps too much of it. The question many analysts quietly ask is whether Taiwan can sustain its edge in high-end manufacturing while geopolitical risks keep rising.

Thailand

Thailand’s growth story feels more cautious. With GDP expected to rise just 2.0% in 2025 and 1.6% in 2026, the country risks slipping behind its ASEAN peers. Low inflation (1.6%) suggests stability, but also lacklustre domestic demand. Political uncertainty and sluggish investment continue to weigh on confidence. It is a reminder that macro stability alone doesn’t guarantee dynamism.

Singapore

Singapore, often seen as the barometer of regional financial health, remains remarkably steady. Growth at 1.9% for both 2025 and 2026 may not turn heads, but it’s paired with near-zero inflation — a rare feat in today’s economy. The city-state’s calm efficiency continues to serve it well, though it may also mask deeper questions about dependence on global finance and trade flows that are becoming less predictable.

Singapore is also at the top of the list of the richest countries in Asia.

The nation’s status as a major financial center in Southeast Asia has attracted multinational corporations, financial institutions, and investment flows. Its emphasis on education, innovation, and research has positioned it as a leader in technology and biomedicine. Singapore’s commitment to sustainable development, coupled with its world-class connectivity and well-developed logistics, enables it to thrive as a trade hub.

Malaysia

Malaysia’s steady 4–4.5% growth looks reassuring on paper. Inflation is subdued, between 1.6% and 2.2%. The challenge, however, lies in sustaining momentum amid global shifts in electronics and palm oil markets — two sectors that have long anchored its export earnings. Policymakers face a delicate balancing act: diversifying without undermining what still works.

Philippines, the 10th largest economy is Asia

The Philippines is one of the region’s brightest spots. Growth is expected to hit 5.4% in 2025 and climb to 5.7% in 2026, with inflation easing below 3.5%. Consumption remains strong, supported by remittances and a vibrant service sector. Still, the economy’s reliance on overseas workers and imported goods makes it vulnerable to shocks — a point that tends to be glossed over in headline figures.

Summary of the top 10 largest economies in Asia in 2025

- China

- India

- Japan

- South Korea

- Indonesia

- Taiwan

- Thailand

- Singapore

- Malaysia

- Philippines

In conclusion, the top 10 largest economies in Asia embody the continent’s dynamism and diversity. From technological powerhouses to emerging giants, each country contributes uniquely to Asia’s economic tapestry. These nations continue to invest in innovation, infrastructure, and human capital. They will also shape the future not only of the continent but also of the global economy.